AI’s Funding Takeover: How 2025 Venture Capital Became a Winner‑Takes‑Most Game

4 min read

Table of Contents

Venture Capital Landscape 2025: The AI-Driven Concentration of Capital

Venture Capital Landscape 2025: The AI-Driven Concentration of Capital

Venture Funding Rebounds with Concentrated Capital Distribution

The venture capital landscape of 2025 reveals a powerful transformation in how investment capital flows into startups. While total venture funding has roared back to life, this capital is being concentrated across dramatically fewer companies, creating a high-stakes environment where mega-rounds dominate the funding ecosystem.

Invest in top private AI companies before IPO, via a Swiss platform:

Swiss Securities | Invest in Pre-IPO AI Companies

Own a piece of OpenAI, Anthropic & the companies changing the world. Swiss-regulated investment platform for qualified investors. Access pre-IPO AI shares through Swiss ISIN certificates.

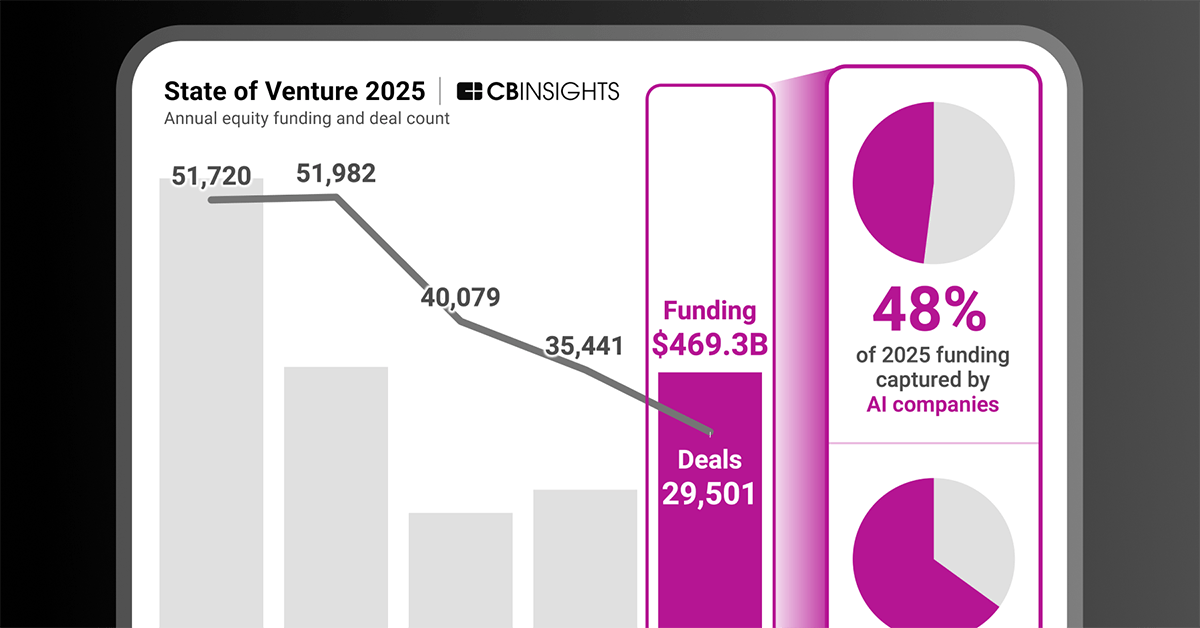

Global venture funding surged to $469B in 2025, representing a remarkable 47% year-over-year increase and reaching the highest funding levels since 2022. The final quarter alone captured $152B, marking the strongest quarterly performance since early 2022. However, beneath these impressive headline numbers lies a more complex and concentrated reality.

Despite the surge in total dollars, deal count actually declined by 17% to 29,501 transactions. Simultaneously, mega-rounds exploded by 77% to 738 deals, capturing a massive $307B and representing 65% of all venture funding. This data reveals that investors are writing substantially larger checks but distributing them to a shrinking group of companies.

AI Dominance Reshapes Investment Priorities

Artificial intelligence has emerged as the overwhelming focal point of venture investment, capturing nearly half of all venture capital in 2025. AI companies raised an extraordinary $226B, accounting for 48% of total venture funding. This represents not merely a trend but a fundamental restructuring of investment priorities.

The six largest funding rounds of 2025 all flowed to AI companies, with these heavyweights collectively raising $111B. This figure represents nearly half of all AI funding and close to a quarter of all venture capital raised worldwide. Five of these companies focus on building and distributing powerful AI models and applications, while others concentrate on building the critical infrastructure that supports AI operations.

This concentration reflects venture capital's massive bet that AI will deliver transformative economic value rapidly enough to justify current sky-high funding levels. If successful, these AI leaders will define the next decade of technology development, business operations, and regulatory frameworks.

Physical AI and Robotics Gain Substantial Momentum

Beyond software-based AI, 2025 marked a breakthrough year for robotics and physical AI systems. Venture investors committed a record $40.7B to robotics, making it one of the top investment destinations alongside AI software. This funding wave focuses on humanoid robots, autonomous vehicles, drones, robot foundation models, and advanced hardware systems.

Physical AI represents AI systems that control physical bodies rather than just processing information. Industrial humanoid robots led all robotics markets with 80 deals in 2025. However, valuations are racing ahead of revenues, with companies like Figure achieving a $39B valuation despite having no revenue stream.

The development of robot foundation models represents a critical breakthrough, serving as general-purpose intelligence systems that can be adapted for specific tasks. These models enable robots to handle complex, unpredictable real-world environments rather than operating only in perfectly controlled settings.

Geographic Concentration Intensifies

Geographic distribution of venture funding has become increasingly concentrated, with US startups capturing $328B in 2025, representing approximately 70% of global funding. This figure approaches the country's 2021 record of $358B. Asia and Europe experienced growth but from substantially weaker foundations, with Asia reaching $53B and Europe approaching $68B.

This geographic concentration reflects deeper structural forces, including regulatory challenges in Asia and Europe's limited number of AI breakthrough companies compared to the United States.

Valuation Explosion Among Elite Private Companies

The top 10 private companies now carry combined valuations exceeding $2 trillion, representing unprecedented levels previously reserved for the largest public technology companies. OpenAI achieved a staggering $500 billion valuation, while Anthropic reached $350 billion, with Anthropic's valuation jumping 19x in a single year.

These valuations reflect market confidence that a small number of AI platforms could dominate substantial portions of future economic activity, though they also raise questions about sustainability and fundamental value alignment.

Leading Investors Concentrate on AI Markets

The world's most successful venture capital firms have dramatically narrowed their focus, with elite "Smart Money VCs" concentrating their investments almost exclusively on AI-related markets. General Catalyst led with 213 deals, followed by Andreessen Horowitz with 178 and Sequoia with 139, but the top 10 markets for these investors were all AI-focused.

This concentration creates a reinforcing cycle where leading AI companies attract increasing amounts of capital, talent, and market attention, further amplifying their competitive advantages and market positions.

The venture capital landscape of 2025 represents a fundamental shift toward concentrated, high-stakes investment in artificial intelligence and related technologies, with profound implications for innovation, competition, and economic development across global markets.

State of Venture 2025 - CB Insights Research

Funding reached its highest level since 2022, with AI nearing 50% of the total. Mega-rounds drove growth. Robotics funding hit record levels. Here’s what happened in venture in 2025.

{kind=link}